ONE signs deal with the USA’s largest electronic health record vendor - 1,100 bed deal already being negotiated

Our Medical tech Investment Oneview Healthcare (ASX: ONE) has just launched a brand new revenue channel…

… and ONE is also already “in contract negotiations on a 1,100-bed opportunity” through that new channel.

(for context - at the end of CY2025, ONE had 14,880 live endpoints across its existing customer base. A 1,100-bed deal would grow the installed bed numbers by almost 10%).

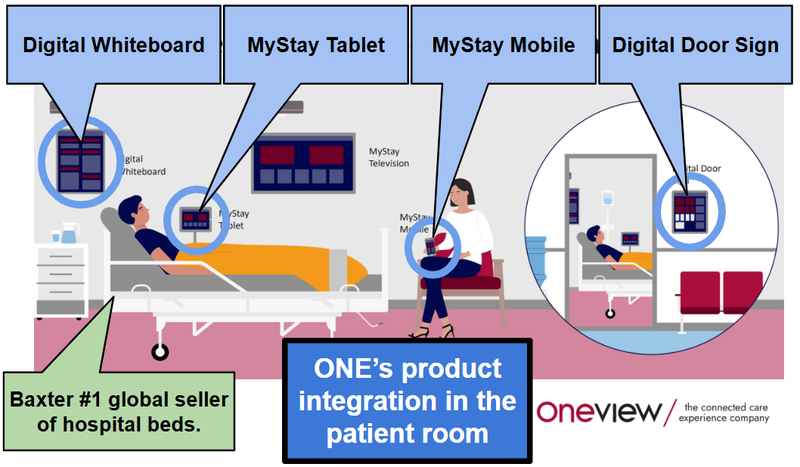

ONE sells software technology to hospitals, along with the hardware to run the systems.

ONE is also developing its own AI powered care assistant - “Ovie”.

Today’s deal opens up a revenue channel for ONE where it would be selling two things - Bedside hardware and a cloud-based device management overlay into the Epic network of hospitals.

Here is some context on Epic’s reach in the US hospital space:

- Epic holds ~42.3% of the US acute care hospital EHR (electronic healthcare records) market (source)

- It represents ~54.9% of all US hospital beds - (source).

- It supports over 305 million patient records (source)

- It is the default platform for virtually all leading US health systems, including major academic medical centres and "Best Hospitals" networks (source)

Here are the areas that Epic covers from their website:

(source)

The deal with ONE would mean all of this gets integrated into ONE managed hardware called “Bedside Hub”.

Put simply, ONE is becoming the infrastructure layer that allows Epic based hospitals to run

The gap the ONE and Epic deal fills

So why would Epic need ONE?

Despite all of the penetration Epic has in the US it doesn’t actually have a fully managed bedside hardware + device + content etc.

Epic is mostly a software company, not hardware.

Enter ONE who can provide that platform:

- TV hardware deployment

- Device provisioning and lifecycle management

- Clinical-grade reliability

- Integration with patient engagement and virtual care workflows

Here is everything ONE sells:

(source)

ONE isn’t competing with Epic, rather it’s becoming an important facilitator of Epic’s next phase of patient engagement and virtual care at the bedside.

Epic’s ~42% hospital market share is concentrated in large enterprise health systems.

These are the ones with the bigger budgets, multi-hospital rollouts and longer contract durations.

Even just a small penetration rate from this agreement could translate into material revenue scale.

For context - at the end of CY2025, ONE had 14,880 live endpoints across its existing customer base. A 1,100-bed deal alone is quite meaningful relative to that base.

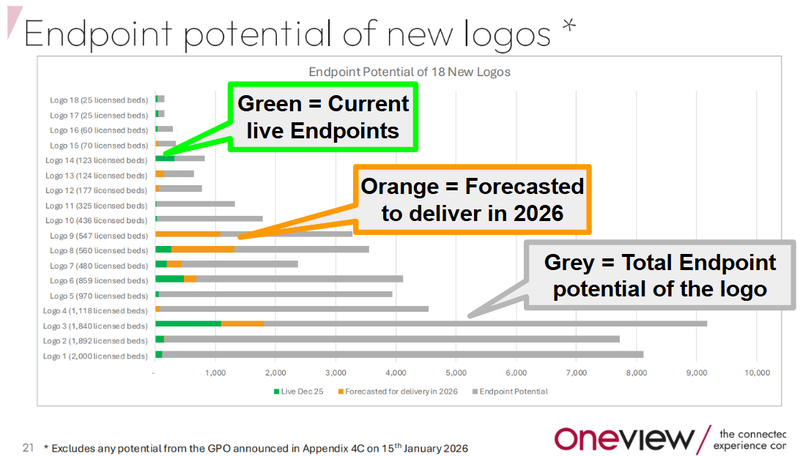

Here is how the pipeline of potential new endpoints was looking earlier in the year:

(source)

What do we want ONE to deliver?

Sales pipeline conversion into signed contracts

ONE had 180+ opportunities and 48,000+ endpoints in its sales pipeline when last provided. We want to see this translate into new signed deals, new customer logos, and accelerating endpoint growth.

Milestones we are tracking:

- ✅ Added to GPO of top-10 US hospital network (January 2026)

- 🔄 First hospital wins from the Top 10 US hospital Group Purchasing Organisation network (confirmed progressing)

- 🔲 New logo wins.

- 🔲 Installed beds converted into multiple “endpoints”.

Rollout of “Ovie” AI services

We want to see the Ovie AI product suite move from announcement to live deployment and start contributing to per-endpoint revenue uplift.

Milestones we are tracking:

- ✅ Ovie digital care assistant unveiled

- 🔲 Ovie customer trials (to begin this year with full rollout during late 2026)

- 🔲 New user experience delivered (H2 2026)

- 🔲 First Ovie-related revenue contribution

Revenue growth and path to breakeven

We want to see ONE continue its consistent growth trajectory and demonstrate a clear path to operating cash flow breakeven.

Milestones we are tracking:

- 🔄 CY2026 live deployment growth of 20% (~17,850 endpoints per guidance)

- 🔄 Continued decline in cash OpEx through 2026

- 🔲 Breakeven achieved

Agreement with Epic

While there wasn’t much in terms of numbers forecasting on how ONE expects this to play out just yet, we are interested to see how this develops.

Epic controls a huge part of the software side of things within the US, so a partnership to help deliver on the hardware side of things could become lucrative.

Epic is a private company with revenues in the range of US$5.7BN for 2024, up from US$4.9BN in 2023. (source)